Financial Market Insight

Highlights

Key Takeaways

- What the U.S./Iran Conflict Means for Markets

- Market Preview: Does the Conflict Stay Contained?

- Economic Cheat Sheet: An Important Week for Growth (Jobs Report on Friday)

- Understanding the Two Sources of AI Anxiety

- Monitoring Private Credit Risk Through Credit Spreads

We normally bring our Financial Market Insight towards the middle of each month; however, because of the increased geopolitical concerns following the U.S./lsraeli conflict with Iran over the weekend, we wanted to get out our immediate thoughts.

As of writing this Monday at 5 AM Oil is up 7%, gold is up 3%, and global stocks are lower as markets price in greater geopolitical risk. However, these moves are right in line with expectations (so currently no worse than feared).

Today's trading focus will be on geopolitics, specifically whether the U.S./Iran conflict widens and expands the number of contributing countries on both sides.

Away from immediate geopolitical concerns, this is an important week for economic data, and the first key report came out this morning with the ISM Manufacturing PMI beating estimates of 51.8, reporting 52.8! Simply put, the stronger this number, the better, as markets need solid growth right now more than they need an earlier than expected interest rate cut. Mid-morning trading seems to appear the strength in economic numbers are prevailing over fear mongering short-term oil prices.

What the Iran Conflict Means for Markets

The U.S and Israel launched a large-scale attack on Iran aimed at regime change, and the operation adds more geopolitical uncertainty to the global markets, although, unless the situation deteriorates, we do not expect it to be a material influence on stocks.

What Happened:

The U.S. and Israel launched a widespread and aggressive missile attack on Iran over the weekend, destroying numerous military sites and killing several of Iran's leaders, including Ayatollah Khamenei. Iran retaliated by targeting U.S. assets across the Middle East.

At this time, the operation is expected to be carried out mostly thought the air without a significant number of troops on the ground, and most expect it will last a few weeks.

What Does It Mean for Markets?

In the near term, the market reaction should be 1) Higher oil and energy prices (including gold) and 2) Lower stock prices on rising geopolitical risks. However, based on current expectations, our investment team does not think the conflict will create sustainably higher oil prices or be a material long term negative on stocks.

We say this for two reasons:

- It is unlikely the attacks will dramatically reduce global oil supplies. Iran is a marginal producer on the global stage, and OPEC announced a production increase over the weekend.

- The effective closure of the Strait of Hormuz will automatically result in tankers avoiding the area for the foreseeable future, which is a near-term negative, but the fact remains that the world is well supplied with oil currently. Without any sustainable increase in oil prices, the conflict is unlikely to impact stocks because there will not be any significant knock-on effects to higher inflation or weaker margins.

What Would Make the Situation Worse?

Further escalation.

- Sustained disruption in Gulf shipping (effective choke point behavior via attacks, closures, or loss of insurability).

- The conflict widens and brings in other countries, then that would be a bearish game-changer and likely create sustainable upward pressure on oil prices, which would be negative for markets.

What Would Make the Situation Better?

Quick resolution! If the operation were to end in the next few days with Iranian military capabilities materially reduced, markets would breathe a relative sigh of relief as fears of further escalation would be removed. Additionally, if there is regime change in the country, that would open the possibility of Iran ultimately returning to the global oil markets, which would increase supply and further pressure prices (good for stocks).

Bottom Line: Despite the dramatic headlines over the weekend, the main influence on stocks remains AI Anxiety, and barring any further escalation in the Iran conflict, that will remain the case. Now, clearly, the conflict is not positive for markets, and it adds to already rising investor concerns; and at a minimum, we can expect more volatility in the near term. However, at its current state, the Iran conflict is not a bearish game-changer (despite any short-term drop), and the medium-term direction of this market is still being determined by 1) AI sentiment, 2) Economic growth, and 3) Fed rate-cut expectations.

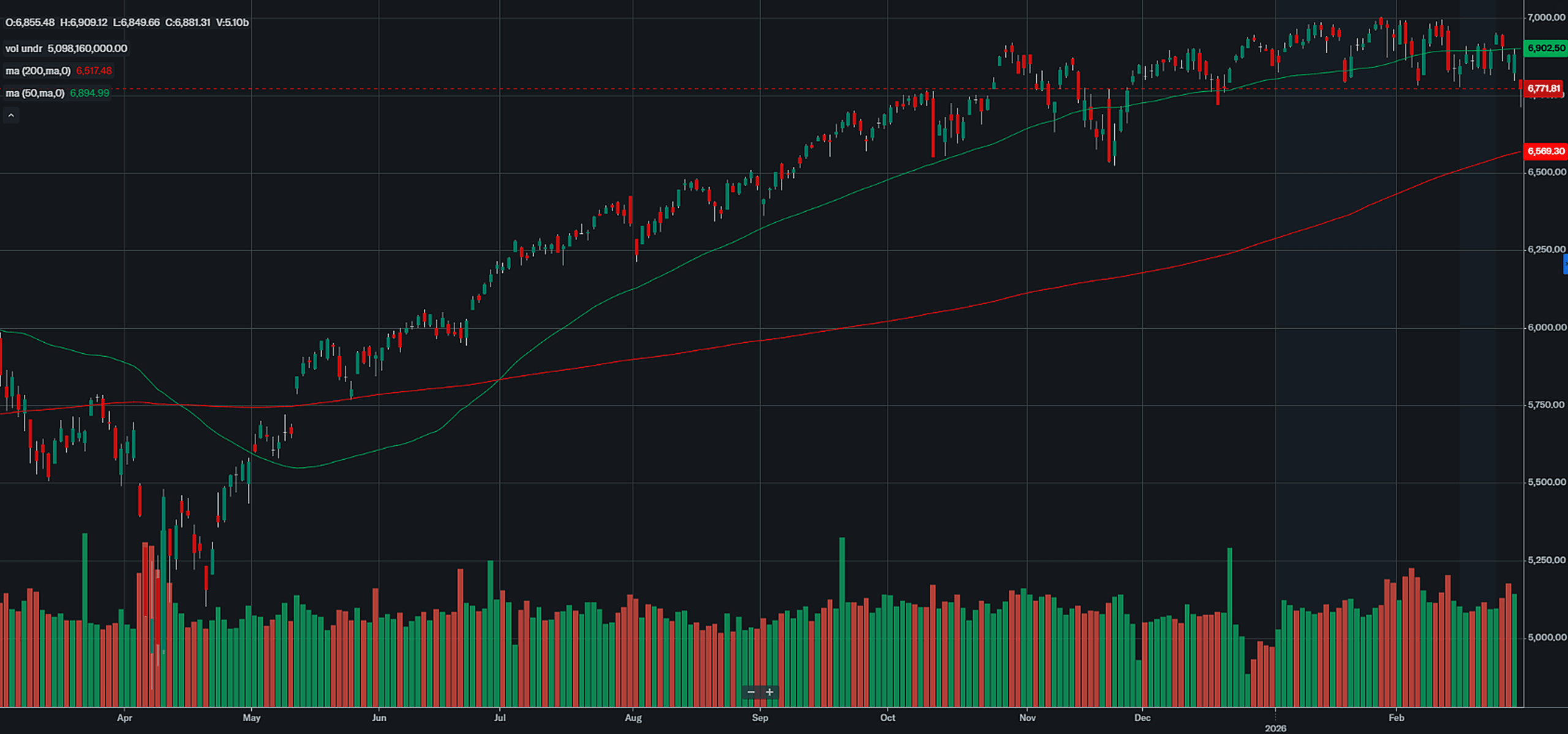

S&P 500 Analysis

S&P 500 Technical Summary

Technical View: The January rally to record highs shifted the technical outlook from cautious to bullish; however, recent volatility has kept conviction notably low.

Primary Trend: Bullish (since Dec 22, 2025)

Key Resistance Range: 6946 - 6975

Key Support Range: 6838 - 6798

Current Level (Reference): 6878.88

"The S&P 500 rallied modestly last week as mixed tech earnings and hopes of an agreement to prevent an attack on Iran offset a jump in inflation metrics."

✓ What is Outperforming: AI-related tech, cyclical sectors, small caps.

✓ What is Underperforming: Defensive sectors, energy.

Economic Data (What You Need to Know in Plain English)

End of February: Data Was Light, Outlook Unchanged

Economic releases were limited and mostly in line, so the outlook stayed the same: solid growth and elevated inflation.

- Jobless claims were essentially on target at 212k vs 215k expected, reinforcing a stable labor market and steady growth, with little market impact.

- PPI was the main surprise: January Core PPI jumped 0.7% vs 0.3% expected, and rose to 4.2% year over year from 3.7%, creating the most disappointing inflation read in months. CPI confirmation will matter.

- Case Shiller home prices rose 0.5% vs 0.3% expected month over month, while 1.4% year over year was in line. Not inflationary by itself, but it suggests the housing-driven disinflation tailwind may be fading, which could keep summer rate cuts less certain.

Bottom Line: Last week did not change the narrative of solid growth with elevated but not reaccelerating inflation, which remains generally supportive of stocks.

March Kick Off: The Big Three, Plus Spending

The start of March has the main monthly reports and a key read on consumers. Markets want confirmation of solid growth without inflation reaccelerating.

- Friday Jobs Report (key event): Markets want a Goldilocks result, solid job gains, but not so strong that rate cut expectations get pushed out. Risks are two-sided, given Fed pushback on near term cuts.

- ISM Manufacturing (today) and ISM Services (Thursday): Both have rebounded and are above 50, signaling expansion. The market preference is in line readings, above 50 but not surging, plus cooling in the price components.

- Retail Sales (Friday): The focus is on whether consumer spending stays steady. A surprise drop in core discretionary spending would raise slowdown risk quickly, but recent trends argue for another solid print.

- Other labor reads: ADP (Wednesday), plus Challenger layoffs and jobless claims (Thursday), round out the picture. A stable labor market supports markets, as long as it is not strong enough to reignite wage inflation and not weak enough to signal deterioration.

SPECIAL REPORTS AND EDITORIAL

Understanding the Two Sources of AI Anxiety

AI anxiety is the dominant near term driver of market sentiment. The concern is no longer whether AI is powerful. It is whether the speed and direction of adoption create unexpected winners and sudden losers. Two forces are doing most of the damage.

The first is sector disruption. The original AI bull case assumed broad productivity gains that lift margins and earnings, especially in white-collar and professional services. Now the fear is more extreme: AI does not just reduce headcount; it can reduce the need for the company itself. Software is the clearest example. Investors initially expected AI to lower costs across engineering, implementation, and support. More recently, the market has started pricing in a world where AI agents and rapid app generation can replicate or replace major software functions with tailored alternatives, compressing pricing power and weakening the moat of many SaaS businesses. Similar concerns have spread into logistics and transportation, where AI-driven routing and automation could push operations toward skeletal staffing models, and into financials, where parts of intermediation and custody may be streamlined.

One way to balance this risk is to maintain exposure to sectors that AI cannot easily replace. A useful framework is HALO, meaning Heavy Assets, Low Obsolescence. These are businesses tied to physical goods and essential services: natural resources, industrial equipment and infrastructure, and core consumer staples. The common thread is simple: AI can optimize processes, but it cannot manufacture barrels of oil, mine copper, build roads, or deliver food on its own.

The second source of AI anxiety is collapsing free cash flow at the largest, most heavily weighted technology companies. For years, many mega-cap platforms generated enormous free cash flow. Now they are deploying massive capital into AI infrastructure, and that spending is materially reducing free cash flow with no clear endpoint. Investors are increasingly uneasy that free cash flow could stay suppressed for years, hinging on a very large bet that AI monetization arrives fast enough to justify the buildout.

Monitoring Private Credit Risk Through Credit Spreads

Concerns about the $1.4 trillion private credit market resurfaced last week when alternative asset manager Blue Owl surprisingly restricted withdrawals from one of its funds and sold off part of the loan portfolio of another fund to raise cash, reviving concerns that the private credit market is teetering and poised to experience potentially painful drawdowns. Blue Owl’s sudden moves reminded investors of First Brands and Tri-Color Holdings, two alternative lenders that suddenly went bankrupt in late 2025.

From a broad standpoint, concerns about private credit have merit. The private credit market has exploded in the past few years, as banks pull back from non-traditional lending, and private pools of capital (private credit) stepped into the market and provided loans at elevated rates, giving investors solid fixed income returns.

In fact, private credit became so attractive that firms moved to provide access to parts of the investing public, changing the funding model of private credit firms from the domain of the very wealthy to now allowing qualified and non-qualified (so retail) investors to allocate to private credit funds via BDCs and public companies like OWL. This influx of capital had to find a home to produce a return (hard to justify private credit management fees with money sitting in cash), and that has spurred fears that private credit has made shaky investments simply to generate returns for investors.

Now, whether that is true, no one knows. Money has indeed flooded into the private credit space and, undoubtedly, some of that money will have “cashed” investments that will go bad. Additionally, it is also true that by letting in a whole new class of investors, it is possible that a lack of understanding of liquidity in private credit could precipitate more funds putting up “gates” to restrict investors from pulling their money.

But whether there is enough of that to become a broader problem is far from known. In the case of First Brands and Tri-Color, those were simply isolated cases. First Brands was run by a dubious executive who had a history of leaving investors holding the bag, while Tri-Color made high-interest but incredibly risky loans, mostly to a portion of the population that was unbanked (due to various reasons). In both cases, there was a lot of risk associated with those investments, and those risks materialized, but they were not emblematic of a broader problem.

And Blue Owl may also be unique. Blue Owl lends heavily to the software industry. So, it is probably more than a coincidence that during a week when many software stocks collapsed to multi-year lows, a lender with broad exposure to the sector also faced stress.

The problem with being able to discern whether the Blue Owl is isolated or a canary in the coal mine is that private credit is a very opaque market. You have to truly be “in it” to have a strong idea of the state of the market. However, while getting that type of access requires being in the industry, the bond market will give us a bit of a “tell” on general credit market stress via credit spreads.

We monitor the Baa/Treasury credit spread, which is basically the “Junk/High Yield” spread minus the same duration Treasury spread. It is an indicator of economic stress and general concern about funding and liquidity.

If we start to see more stress in private credit, then this spread will begin to widen sharply and quickly, and that will be a sign that contagion is starting to appear. And that would be demonstrably negative for markets. Thankfully, there are no signs of that occurring. The Baa credit spread currently sits at 1.73%, which is up slightly from the lows of the year at 1.59%, but well off the one-year highs of 2.02% last April.

If the Baa credit spread rises solidly above 2.00%, that will be a sign that stress is emerging about private credit or some other funding source, and that will get our attention. We will continue to monitor credit spreads for any sign of that increase.

For now, the bond market is not signaling that private credit is in trouble, although it is something we all have to monitor, because the ingredients for a problem are there (too much money chasing limited quality return opportunities).