Financial Market Insight May 12, 2026

VANN EQUITY MANAGEMENT

Financial Market Insight

Market Rally: Strong Fundamentals, But Real Risks Remain • Market Preview: Does the ceasefire finally happen? • Economic Cheat Sheet: A big week for inflation • Why the Consumer Remains Resilient: Low Unemployment

HIGHLIGHTS

Market Rally: Strong Fundamentals, But Real Risks Remain

Market Preview: Does the ceasefire finally happen?

Economic Cheat Sheet: A big week for inflation

Why the Consumer Remains Resilient: Low Unemployment

V

STOCKS

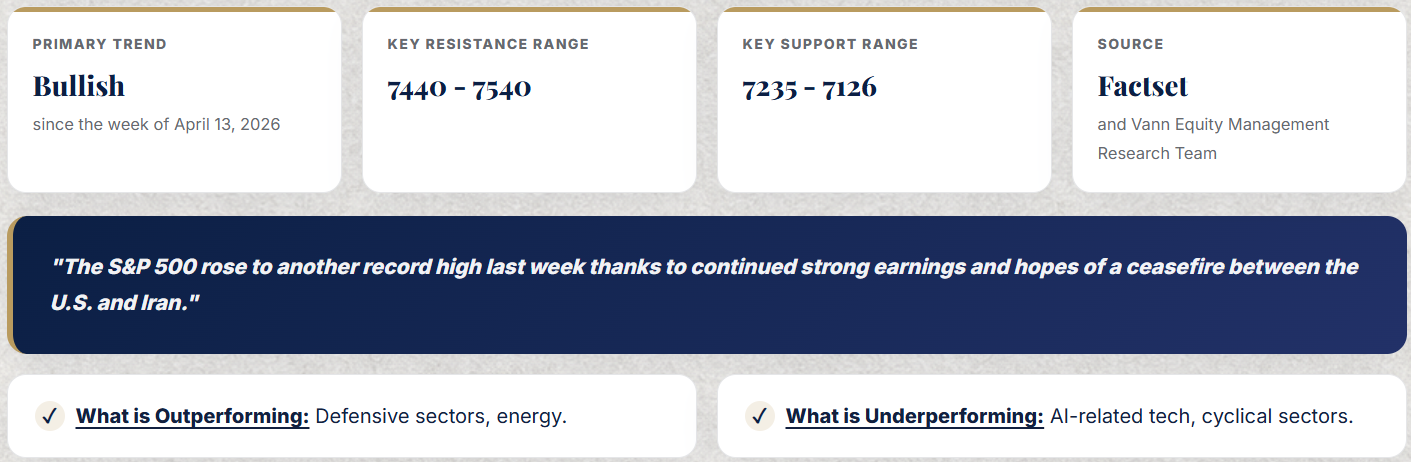

S&P 500

Technical View: The S&P 500 surged to new record highs in mid-April, shifting the primary trend back to bullish but amid a sense of caution regarding sustainability.

SOURCE: Factset and Vann Equity Management Research Team

✓What is Outperforming:Defensive sectors, energy.

✓What is Underperforming:AI-related tech, cyclical sectors.

Market Commentary

Market Rally: Strong Fundamentals, But Real Risks Remain

The market rally over the past six weeks has been impressive, not only because of its size, with the S&P 500 rising nearly 20% from its recent low, but also because the rally has had fundamental support behind it.

Two key factors have helped underwrite the move higher:

Very strong earnings growth

Resilient economic data

That combination has created a constructive macroeconomic backdrop. However, a strong market is not the same thing as an invincible market. While the current setup remains positive, several meaningful risks remain on the horizon.

The purpose here is not to focus on normal short-term pullbacks. A 3% - 5% decline is part of ordinary market behavior."Instead, the focus is on larger risks that could threaten the durability of this rally and potentially change the broader market outlook".

Risk 1: Stagflation Becomes a Reality

The primary concern behind the March market decline was that rising energy prices could eventually createstagflation, which is the difficult combination of slow economic growth and high inflation.

So far, that has not happened. Inflation pressures have moved higher, but economic growth has remained resilient. In other words, the economy is still running hot, with solid growth and elevated prices occurring at the same time.

Much of the recent inflation pressure has been tied to energy and commodity prices. The market expectation is that if geopolitical tensions ease and energy prices decline, the recent inflation spike could prove temporary.

However, the key issue is not just the intensity of the price increase. It is the duration.

The U.S. consumer was already facing affordability pressure before the latest increase in energy and commodity prices. Higher fuel, food, and input costs only make that burden heavier. So far, consumers have been able to absorb the pressure, but the longer prices remain elevated, the greater the risk that inflation becomes more deeply embedded across the economy.

Unlike the COVID period, households are not receiving large stimulus checks or benefiting from forced savings. That means there is less financial cushion to offset higher everyday costs.

If energy and commodity prices stay elevated for several months, broader price pressures could return. If that happens while growth begins to slow, stagflation could become a real risk later this year. That would be a negative outcome for both stocks and bonds.

Risk 2: The Fed Is Forced to Raise Rates Again

There are several comparisons being made between today's environment and the 1970s. One potential similarity is the risk that the Federal Reserve may eventually have to raise rates again after previously cutting them.

For now, the Fed appears to view much of the recent inflation pressure as temporary and largely tied to energy prices. But the longer elevated prices persist, the more concerned Fed officials may become about a broader inflation rebound.

We are already seeing signs of a more cautious and hawkish tone from the Fed. While both rate hikes and rate cuts remain relatively low probability outcomes, the market has recently assigned a higher probability to a rate hike than a rate cut by year's end.

If the Fed were forced to begin another rate-hiking cycle, it would likely put additional pressure on economic growth. Higher rates, combined with elevated inflation, could increase the risk of a sharper slowdown.

That is a dangerous combination for the market. The last time the Fed had to aggressively raise rates to control inflation, the S&P 500 declined more than 20%.

Risk 3: The AI Boom Slows or Breaks

The first quarter earnings season was undeniably strong, and that is an important positive for the market. However, a meaningful portion of the earnings strength has been tied to the artificial intelligence boom.

The AI investment cycle is being driven by massive capital spending from a relatively small group of large technology and infrastructure companies. That spending has directly benefited technology companies through demand for semiconductors, servers, cloud infrastructure, and data center equipment.

But the impact has extended beyond technology. The data center buildout is also supporting industrials, real estate, utilities, materials, and other areas of the economy. In many ways, AI-related capital spending has become a major private sector stimulus program.

That is powerful, but it is also concentrated.

If AI-related spending slows materially, the same force that has helped lift earnings and economic activity could quickly become a drag. What has been exporting an economic boom could begin exporting and an earnings slowdown.

That would create a double risk for stocks. First, market multiples could fall as investors reassess future growth expectations. Second, the most important sector leadership group in the market could come under pressure at the same time.

The Bottom Line:

None of these three risks appears imminent, and the market remains fundamentally supported by strong earnings and resilient economic growth.

But that does not mean investors should ignore what could go wrong.

Stocks can decline in a sustained way. It may not feel like that in the middle of a powerful rally, but durable market reversals do happen. Our job is not to become permanently bullish or permanently bearish. Our job is to remain clear-eyed. That means participating in the strength when the fundamentals support it, while also staying aware of the risks that could change the outlook.

By identifying these risks now,we can avoid two mistakes:

Sounding like permanent bulls who dismiss legitimate concerns

Being caught off guard if the market environment turns more negative

For now, the rally deserves respect. But so do the risks.

Economic Data

Economic Data (What You Need to Know in Plain English)

The economic data this month continues to send a broadly constructive message: growth remains solid, the labor market remains healthy, and overall activity is still strong enough to support the market rally.

The most important data point was the jobs report, which came in stronger than expected and was close to a Goldilocks outcome. The economy added 115,000 jobs versus expectations of 65,000. That is strong enough to confirm continued economic momentum, but not so strong that it would likely force the Fed into a more aggressive stance.

Other parts of the labor report told the same story. The unemployment rate held steady at 4.3 percent, while wage growth slowed to 3.6 percent year over year from 3.8 percent. That combination is important. Stable unemployment suggests the labor market remains healthy, while slower wage growth helps reduce pressure on inflation.

Other labor market indicators also remain solid. Jobless claims rose to 205,000, but that is still historically low and well below the 260,000 level that would begin to raise concern about labor market weakness. Job openings, as measured by JOLTS, remained stable at 6.9 million. That is well below the post-pandemic highs, but still comfortably above the sub-six-million level that would suggest real deterioration.

In plain English, the labor market is cooling but not cracking. That is exactly what investors want to see.

Growth data also remains supportive. The ISM Services PMI slipped modestly to 53.6 versus expectations of 53.9, while New Orders declined to 53.5 from a very elevated 57.5. Those were softer readings, but they remain comfortably above 50, which means the service sector is still expanding.

That matters because services represent the majority of the U.S. economy. As long as service sector activity remains in expansion, broader economic growth should remain supported.

The concern, however, remains inflation.

The Prices Paid index stayed elevated at 70.7, matching one of the highest readings since 2022. While it is encouraging that the index did not move higher, the current level still suggests that companies are facing meaningful cost pressures. The last time this index was near these levels, CPI was running above 6%.

That does not mean inflation is about to return to those levels, but it does mean investors should not dismiss the risk.

For now, the market is focused more on the strength of economic growth than the risk of sticky inflation. That is why the current environment still looks supportive of stocks. However, if inflation data begins to move higher again, that could put upward pressure on yields and increase the probability of a Fed rate hike later in 2026.

The key inflation readings this month will be CPI and PPI. The headline CPI number will be important, especially because it reflects another full month of elevated energy prices. Although the more important figure will be Core CPI, which excludes food and energy. Core CPI was 2.6% year over year in the prior report. If it moves closer to, or above, 3%, that will likely make Fed officials more cautious and could become a mild headwind for stocks.

Consumer spending will also be important to watch. Retail sales will provide a clearer view of household demand, but the key number will be the Control Group, which gives better insight into discretionary spending. Since consumer spending is the engine of the U.S. economy, continued resilience would help push back against stagflation concerns.

Finally, the Empire Manufacturing survey will offer an early look at the current month's activity. It is a volatile regional report, so it should not be overread, but it can still provide useful insight into manufacturing activity, pricing pressure, and the effect of elevated energy costs.

The Bottom Line:

The economic backdrop remains favorable. Growth is solid, the labor market is cooling gradually, and consumer activity has not shown signs of breaking.

That is supportive of the market.

The risk is that inflation pressure remains too sticky for too long. If inflation continues to rise while growth slows, stagflation concerns could return quickly. That is one of the few risks that could seriously challenge this rally.

For now, the data still supports the market. But inflation remains the number to watch.

Special Reports and Editorial

SPECIAL REPORTS AND EDITORIAL

Why the Consumer Remains Resilient: Low Unemployment

The first-quarter earnings season reinforced one of the most important themes supporting the economy and the market: the U.S. consumer remains resilient.

Companies tied directly to personal finance, including banks and credit card companies, continued to report healthy consumer activity. Companies tied to discretionary spending, including restaurants, travel, and apparel, also showed that demand remains firm despite higher prices and a volatile start to 2026.

The main reason is simple: people still have jobs.

Consumer spending is not just an abstract economic data point. It is the lifeblood of the U.S. economy. More than 60 percent of U.S. economic activity is driven by consumer spending, which is why analysts pay close attention to Personal Consumption Expenditures in every quarterly GDP report.

If consumer spending weakens, economic growth usually follows. In plain English, as the consumer goes, so goes the U.S. economy.

There have been legitimate concerns that consumers would eventually pull back under the weight of higher prices. Inflation has already pressured household budgets, and the recent rise in oil and gasoline prices adds another burden. But discretionary spending has remained stronger than many expected.

Again, the reason is straightforward: steady employment supports steady spending.

As long as Americans have jobs and a reliable income, they are much more likely to keep spending, even when prices are elevated. The real problem begins when job losses rise, and income becomes uncertain. That is when households begin to cut back more aggressively.

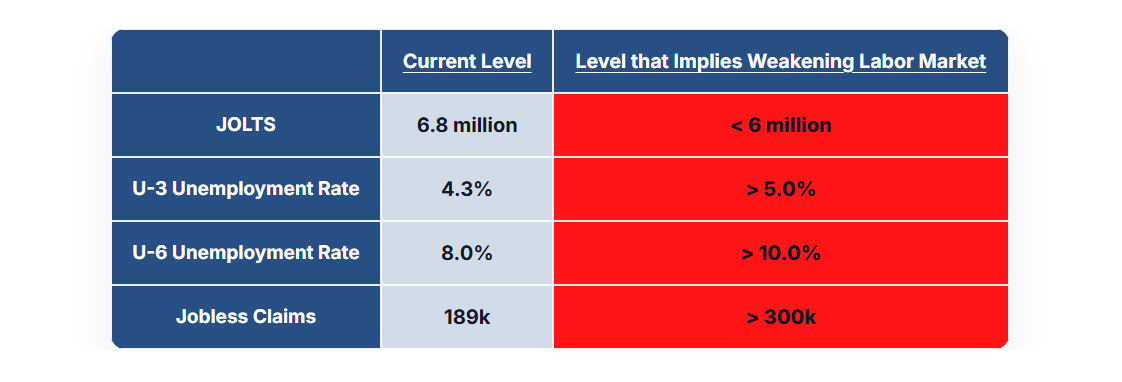

Despite ongoing concerns that artificial intelligence could eventually pressure employment, the current labor market data is telling a very different story. Virtually every major labor market indicator we track still points to a healthy employment backdrop.

Job openings, as measured by JOLTS, are well below the post-pandemic highs, but they remain stable at 6.8 million. That is not a booming labor market, but it is also not a labor market in trouble. Importantly, job openings remain comfortably above the sub-6 million level that would suggest employers are moving toward a hiring freeze.

The unemployment rate also remains historically low. The most commonly followed measure, known as U3 unemployment, sits at 4.3 percent. That is above the post-pandemic lows, but still well below the 5 percent level that would begin to signal broader weakness in the labor market.

The broader U6 unemployment rate, often referred to as the underemployment rate, tells a similar story. This measure includes unemployed people as well as people who want more work but cannot get it. At 8.0 percent, U6 recently hit its lowest level since September and remains well below the 10 percent level that would indicate meaningful labor market stress.

Weekly jobless claims, which are one of the highest frequency indicators of labor market conditions, also remain very low. Claims recently fell to 189,000, a historically strong number and still nowhere near the 300,000 level that would suggest a serious rise in layoffs.

The Bottom Line:

The consumer remains resilient because the labor market remains healthy.

That matters a lot about this rally.

If employment remains strong, consumer spending should remain supported. If consumer spending remains supported, the economy is unlikely to lose momentum quickly. And if economic growth remains solid, the probability of a sustained market decline or bear market remains lower.

This does not mean the consumer is immune to pressure. Higher prices, elevated borrowing costs, and rising energy expenses are real headwinds. But as long as the labor market holds together, the foundation under consumer spending should remain intact.

For now, the message from the data is clear: the labor market is not cracking, and that remains one of the strongest supports for the economy and the stock market.

Disclaimer: The Financial Market Insight is protected by federal and international copyright laws. Vann Equity Management is the publisher of the newsletter and owner of all rights therein and retains property rights to the newsletter. The Financial Market Insight may not be forwarded, copied, downloaded, stored in a retrieval system, or otherwise reproduced or used in any form or by any means without express written permission from Vann Equity Management. The information contained in Financial Market Insight is not necessarily complete, and its accuracy is not guaranteed. Neither the information contained in Financial Market Insight, nor any opinion expressed in it, constitutes a solicitation for the purchase of any future or security referred to in the Newsletter. The Newsletter is strictly an informational publication and does not provide individual, customized investment or trading advice. READERS SHOULD VERIFY ALL CLAIMS AND COMPLETE THEIR OWN RESEARCH AND CONSULT A REGISTERED FINANCIAL PROFESSIONAL BEFORE INVESTING IN ANY INVESTMENTS MENTIONED IN THE PUBLICATION. INVESTING IN SECURITIES, OPTIONS, AND FUTURES IS SPECULATIVE AND CARRIES A HIGH DEGREE OF RISK, AND SUBSCRIBERS MAY LOSE MONEY TRADING AND INVESTING IN SUCH INVESTMENTS.